Thought of the week – How do practitioners use ESG data?

To me, it is always interesting to see what investment practitioners think about ESG and how they use it in practice. No wonder then that I like a new survey by Franck Bancel and his colleagues involving 303 mostly French portfolio managers, financial analysts, ESG specialists, and company valuation experts.

First, one result that didn’t surprise me, but which flies in the face of claims by many investment banks and sell-side brokers, is that the people who use ESG data to value companies and assess their risks are predominantly portfolio managers and investment specialists on the buy side. Neither sell side analysts nor investment bankers are statistically significantly likely to use ESG data in their jobs, confirming what I talked about here.

But apart from confirming my suspicions about some groups of investors, the really interesting results are the ones about the quality of ESG data, how ESG data is used by investment practitioners and how it influences the valuation of companies, in their view.

First, the number-one complaint about ESG data remains the lack of standardisation. In the survey, 86% of respondents said that ESG data is not sufficiently standardised. As a result, two out of three investors use an internally developed ESG scoring system to value companies. If you can’t trust third-party systems for ESG ratings, you have to build one yourself… In this respect, I find it notable that only one out of three investment practitioners use more than two ESG data providers. This seems a marked decline from past surveys that I have seen, where investment practitioners typically used three or four data providers. I suppose there were many specialist data providers that have been abandoned in favour of the two or three major full-service providers in the market.

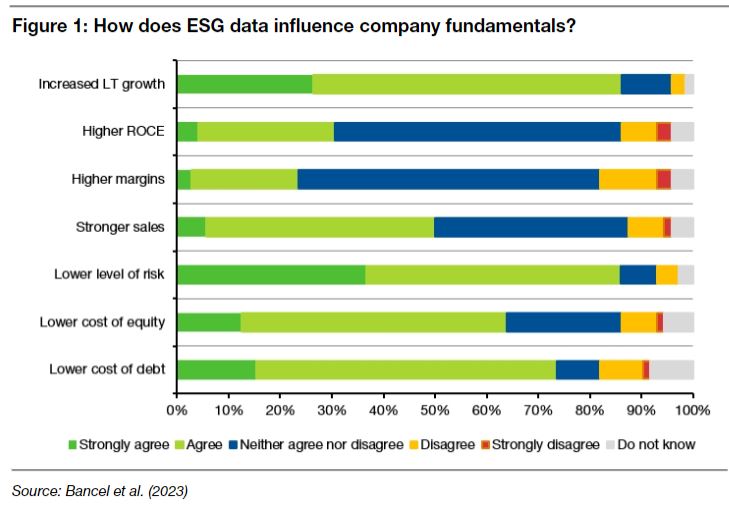

When it comes to the relevance of ESG data on company fundamentals, there is a broad consensus that better ESG performance leads to:

• Lower cost of debt (I agree, there is plenty of empirical evidence that supports this notion).

• Lower cost of equity (the empirical evidence on this is mixed, but from what I have seen there is some weak evidence that better ESG performance reduces the cost of equity).

• Lower level of risk (this to me is the number-one reason why you want to include ESG analysis in your investment process).

• Increased long-term growth and higher sales (I disagree, I think there is a lot of wishful thinking in terms of better ESG performance leading to higher market share or higher long-term growth).

At the same time, there seems to be agreement among most investment practitioners that better ESG performance does not lead to higher margins or higher return on capital employed, and I agree with this assessment.

The survey get really interesting when it asks practitioners how ESG analysis influences their company valuation models. Here, the most common approach is not to adjust cash flows (though about 40% of respondents do that, as well), but to adjust the discount rate of future cash flows and the long-term growth rate. Essentially, ESG analysis provides a risk and opportunity assessment for a company and the risks are reflected in higher risk premiums in the discount rate, while opportunities are reflected as higher long-term growth rates. And that seems eminently sensible to me.

Thought of the Day features investment-related and economics-related musings that don’t necessarily have anything to do with current markets. They are designed to take a step back and think about the world a little bit differently. Feel free to share these thoughts with your colleagues whenever you find them interesting. If you have colleagues who would like to receive this publication please ask them to send an email to joachim.klement@liberum.com. This publication is free for everyone.